Royal Mail PLC (RMG) have announced they will introduce Sunday parcel deliveries nationwide in the efforts to keep up with Amazon. Will this keep their share price bullish when lockdown ends?

From next month, Royal Mail will deliver parcels across the UK seven days a week in response to the high demand of online shopping over the pandemic. The service will allow customers to specifically request delivery on Sundays from retailers who use Royal Mail.

Royal Mail is making efforts to future proof their service with new CEO Simon Thompson making that his focus. He also aims to maintain good relations with trade unions. One of his first moves was to broker an agreement with the CMU on the employee pension scheme and cut the working week by 1 hour which could save £225 million per year. And when the company saves, the investor gains.

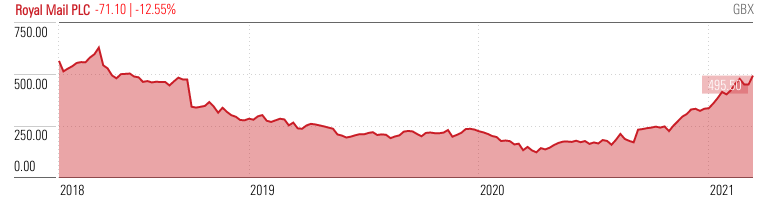

The Royal Mail share price has risen by 175% since September 2020. While share price increases were expected from the start of the pandemic last spring due to a surge in parcel volumes, the company has surprised analysts with the rate of recent gains. RMG has certainly made a comeback following a slow decline in share price over recent years.

In Q4 of 2020, Royal Mail delivered 496 million parcels, which is an all-time record for the company. The consumer shift towards e-commerce and online shopping has resulted in a massive increase in parcel delivery whilst a 14% decline in letter delivery over Q4 was found. To keep up with demand, Royal Mail has kept on 10,000 of the 33,000 temporary staff hired to cover the hectic festive season suggesting things are looking up.

An estimated profit of £500 million in 2020 equates to an outstanding 78% year-on-year growth rate.

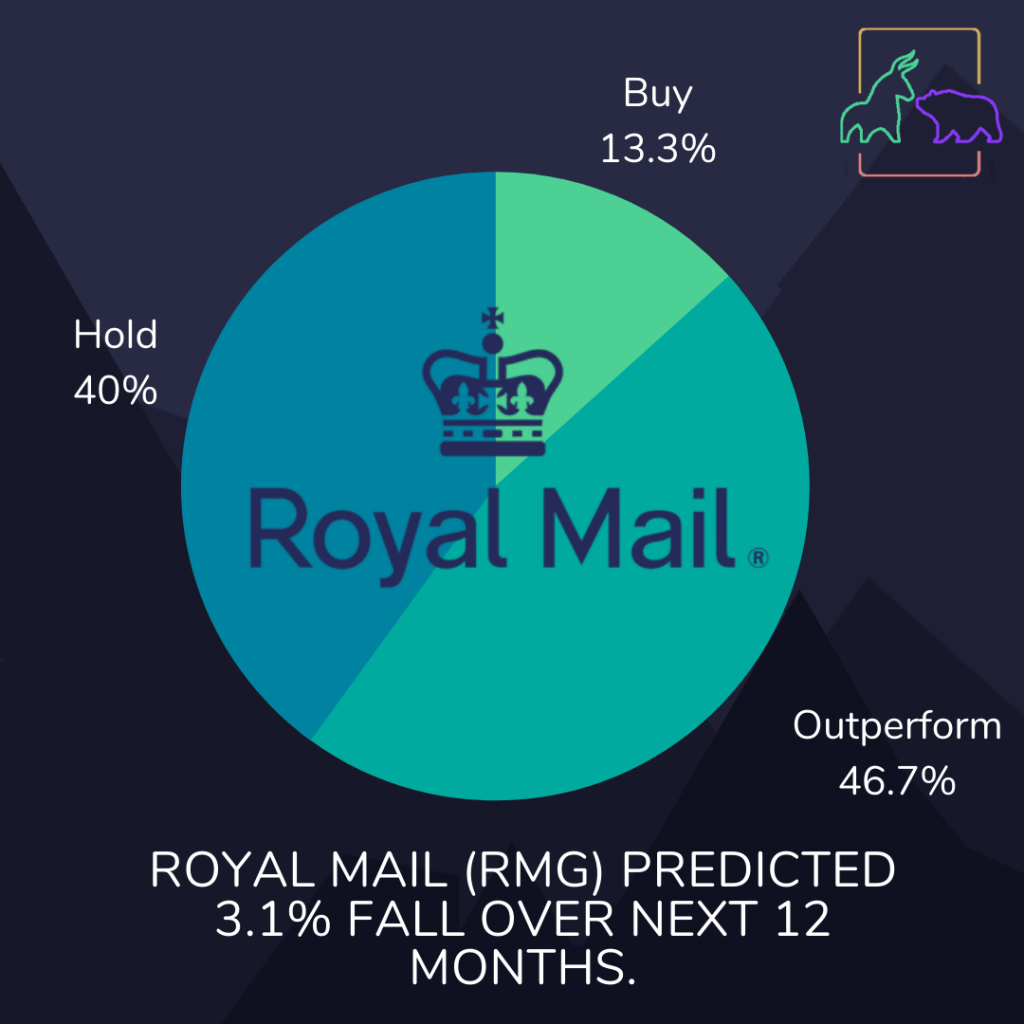

The Financial Times’ analysts saw RMG as an outperformer. The outperform rating means the company will produce a better rate of return than similar companies but is not the best stock out there in the industry.

Before you invest in RMG, you will need to open an account with a broker to manage your investments.

Choosing the best online stock broker can make the difference from an easy and exciting new experience to constant frustration and disappointment. Accessing financial markets through online brokers is easy and inexpensive but there are so many out there tailored to a different sort of customer so choose the right broker that will optimise your user experience and profits.

If you’re just starting out we recommend eToro and easyMarkets for their easy to use interfaces and fee – free trading.

Price Forecast

Over a year, the Royal Mail stock price are expected to fall slightly. The 15 analysts offering 12 month price targets for Royal Mail PLC have a median target of 480.00, with a high estimate of 708.00 and a low estimate of 284.00. The median estimate represents a -3.13% decrease from the last price of 495.50.

If you are interested in dividends it doesn’t look good. In 2020, Royal Mail PLC reported a dividend of 0.08 GBP, which represents a 70.00% decrease from last year. The 9 analysts covering the company expect dividends of 0.05 GBP for the upcoming fiscal year, a decrease of 40.00%.

With the pandemic coming to a close, will online shopping produce enough parcels for Royal Mail to stay bullish? If you are ready to invest, we recommend eToro and easyMarkets for beginners.

Let’s celebrate International Women’s Day together. In a male-dominated world it is important to recognise female role models to inspire women to enter the world of finance. Here are five inspirational female investors who rose to the top of the finance industry.

Finance is a strongly male-dominated industry with only 19% of senior positions in the investment sector held by women (according to Catalyst Research). Entering the world of finance as a woman can be challenging, employers can underestimate, expect unreasonably high standards and be opposed to hiring us all together. The role models we will introduce go above and beyond expectations and with hard work and grit they are willing to stand out and take risks to make it in finance.

Considering women make up 50% of the world population it is crucial to include women in the workplace to raise the economic potential of a country. Inequalities have long been a barrier for women to participate in business, finance is among the top sectors for gender discrimination.

Geraldine Weiss was one of the first women to become big in finance. She grew her success by self-learning before studying business and finance. When applying to investment firms after her studies she was rejected multiple times despite being more than qualified for the role. She commented “It was a man’s world, and women need not apply,”.

After a series of rejections, Weiss decided to start her own investment newsletter in 1966. To avoid further gender discrimination, Weiss signed her newsletter “G. Weiss.” She only revealed her gender identity a decade later after proving her strategies were a huge success.

Her newsletter, Investment Quality Trends is still going today, based on Weiss’s incredibly successful value-based, dividend-oriented stock-picking strategy.

Muriel Siebert

Muriel Siebert entered the world of finance as a researcher before climbing the ranks to partner before starting her own brokerage firm Muriel Siebert & Co. in 1967.

Siebert was determined to get her firm registered with the NYSE facing numerous rejections. Eventually she succeeded and her firm became the first woman-owned member of the NYSE. It is still the only national, woman-owned brokerage on the exchange.

Siebert didn’t stop there and went on to bring her financial expertise to politics, another male-dominated field. As New York State Banking Department Superintendent from 1977 to 1982, in a rocky market, she helped prevent bank failures to support the US economy.

Abby Joseph Cohen

Abby Joseph Cohen served as a Federal Reserve Board economist in 1973 before moving to work for firms such as T. Rowe Price, Barclays, and Drexel Burnham Lambert. In 1990 she joined Goldman Sachs and became a partner just 8 years later.

Cohen was listed on Forbes‘ “Most Powerful Women” celebrating successful women across all professions.

Lubna S. Olayan

Lubna Olayan probably faced the most challenging cultural barriers of all our women in finance. As a Saudi women, it is not socially acceptable for women to work let alone work in business, and back in the 80’s! Olayan gained support from her family and overcame gender discrimination to become CEO of Riyadh-based Olayan Financing Company, one of Saudi Arabia’s most prominent companies. She now employs more than 540 women in her company and constantly campaigns women in the workforce.

Linda Bradford Raschke

Last but not least, we explore Linda Raschke’s achievement to become president of not one, but two financial firms that bear her initials: LBRGroup, Inc. and LBR Asset Management. After kicking off her career in the early 80’s Raschke has constantly challenged a male-dominated workforce. Starting as a market maker and then becoming a day trader Raschke has had all the experience needed to write her popular book on high probability trading strategies. She has also lectured on trading at Bloomberg.

Being a woman in finance means high pressure, but also high visibility. Many women in finance still face gender discrimination and lower pay for comparable work. Take inspiration from these women to start changing a male-dominated industry. If you are ready to start trading, we recommend eToro and easyMarkets for beginners.

Abbott Laboratories has just got emergency use authorisation from the U.S. health regulator or its molecular test to detect and distinguish the coronavirus and two types of flu viruses with a single test. Will this set a bright future ahead for the medical company?

Shares of Abbott Laboratories (ABT) slid 2.66% to $116.01 Thursday, a rough trading session for the stock market, which saw the S&P 500 Index falling 1.34% to 3,768.47 and Dow Jones Industrial Average falling 1.11% to 30,924.14. Abbott Laboratories closed $12.53 below its 52-week high ($128.54), which the company achieved on February 12th.

The stock underperformed when compared to some of its competitors Thursday, as Johnson & Johnson fell 2.02% to $153.07 and Pfizer Inc. fell 0.55% to $34.20. However, with the announcement today if a new test being launched in the US will the stock make a strong recovery?

Abbott Laboratories announced the U.S. health regulator has granted emergency use authorization for its molecular test to detect and distinguish the coronavirus and two types of flu viruses with a single test, which can also be used worldwide. This is crucial to diagnosing and managing COVID-19 as the viruses present similar symptoms but require different treatment approaches.

Company Performance

So now you know why today we are focusing on ABT stock lets take a look at the company’s performance.

Abbott Laboratories set a record high in 2020 benefiting from their wide range of successful coronavirus tests.

In December, the company announced the FDA granted its BinaxNOW Covid-19 an emergency use authorization for at-home use. This meant the rapid antigen test was allowed for use in the home, where previously not allowed. ABT has supplied over 180 million BinaxNOW COVID-19 tests to this date.

In the fourth quarter, sales surged 28.7% to $10.7 billion, with adjusted earnings of $1.45 per share soaring a massive 52.6%. Considering these reports were mid coronavirus pandemic, diagnostic sales soared 108.9% to $4.35 billion and coronavirus testing contributed $2.4 billion in the quarter. This means medical device sales have slightly dropped, although not surprisingly considering the delay in elective procedures during the pandemic.

Overall Abbott Laboratories’ contribution to tackling the global pandemic has set them in good stead recently. Over the past few months analysts have recommended to BUY, we would like to suggest the current dip and recent announcement as the perfect opportunity to BUY that will give a slight edge over the longer trend seen.

Before you invest in ABT, you will need to open an account with a broker to manage your investments.

Choosing the best online stock broker can make the difference from an easy and exciting new experience to constant frustration and disappointment. Accessing financial markets through online brokers is easy and inexpensive but there are so many out there tailored to a different sort of customer so choose the right broker that will optimise your user experience and profits.

If you’re just starting out we recommend eToro and easyMarkets for their easy to use interfaces and fee – free trading.

Price Forecast

The 17 analysts offering 12-month price forecasts for Abbott Laboratories have a median target of 137.00 representing a +18.14% increase from the last price of 115.96.

It’s worth noting that Abbott’s earnings and sales gains in the fourth quarter are expected to repeat in the first quarter. Although with the pandemic being better controlled each day, keep an eye on the need for coronavirus testing.

The overall recommendation is to buy stock in Abbott Industries. Their success through the pandemic and strong R&D bringing out new types of COVID-19 test regularly puts the company in a strong position of growth. If you are ready to invest, we recommend eToro and easyMarkets for beginners.

After last week’s explanation of how candlesticks are formed and how to interpret them we can now explore what the most common candlestick patterns can indicate. Start analysing charts before you enter a trade, it will almost certainly pay off!

How to analyse a trend

The trend whether up or down can be demonstrated using trend lines, moving averages or other tools as part of technical analysis. It is important to consider the timeframe you are using as what seems like a trend on a 1minute chart is irrelevant if you are looking to hold your position for a few days, it would be better to look at a 30 minute chart, although this is really up to an individual.

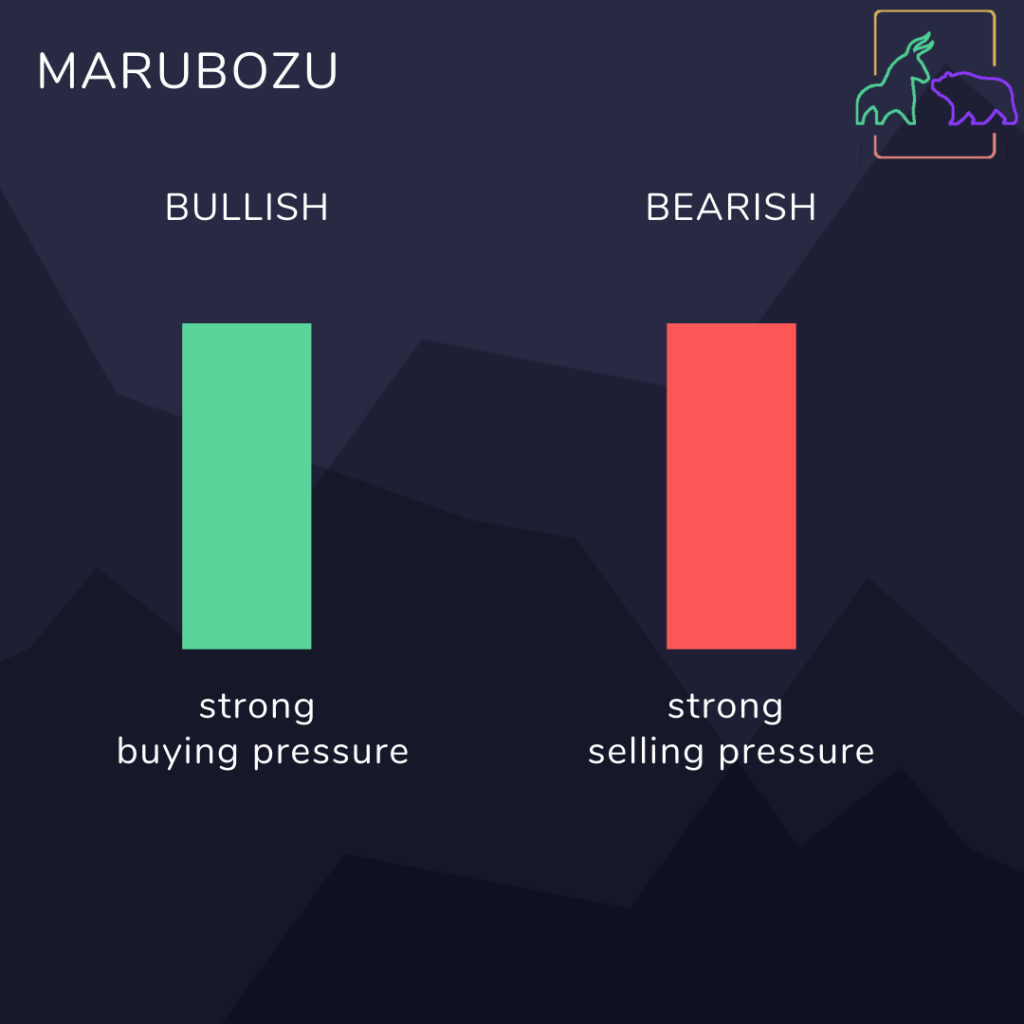

A Marubozu candlestick is a long candlestick that does not have upper or lower shadows (wicks or tails). This occurs when the low and high are inline with the opening and closing prices presenting either buyers or sellers (depending on whether the candle is green or red) exclusively are strongly in control of the price over the period. A green Marubozu forms when the open equals the low and close equals the high whereas a red Marubozu forms when the close equals the low indicating a very strong buying pressure and the open equals the high presenting a very strong selling pressure.

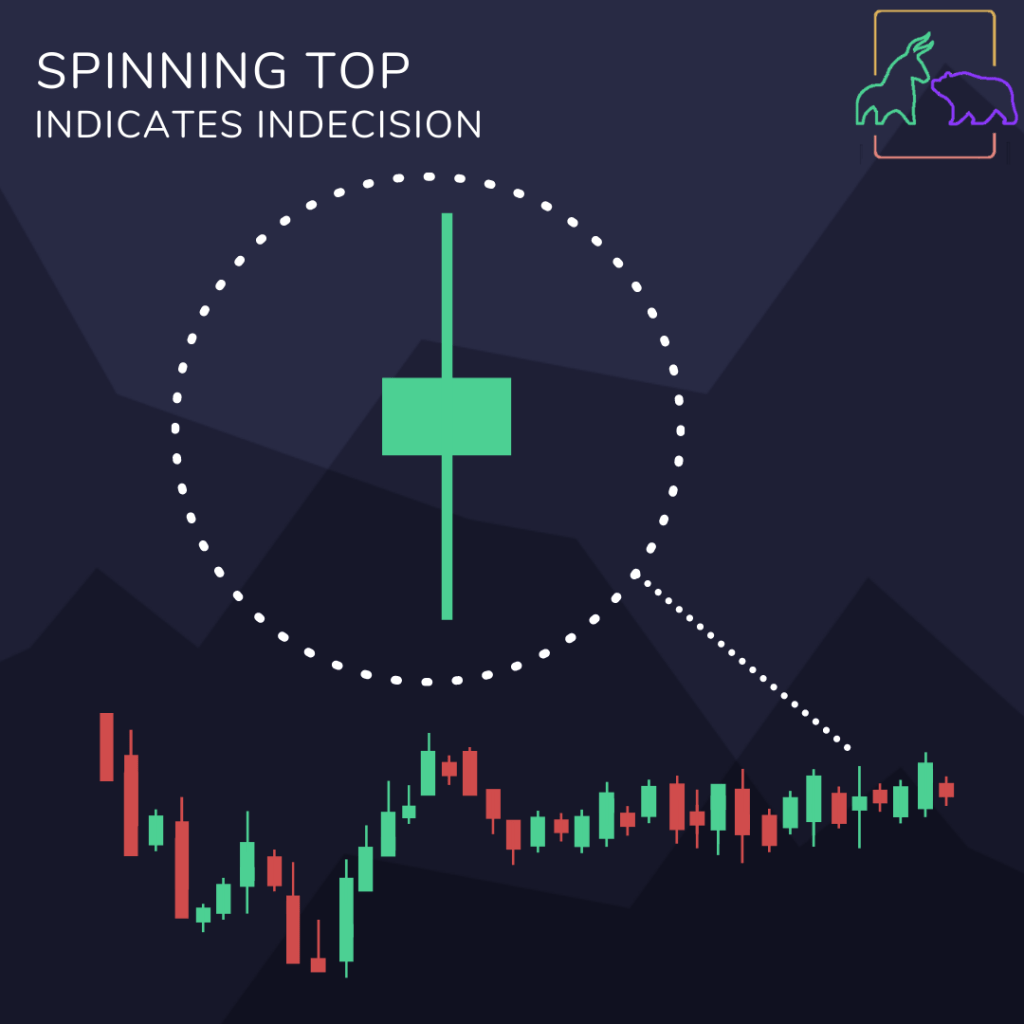

Spinning tops are candlesticks with a long upper and lower shadow with a small body. Spinning tops represent indecision as the small body represents little movement in price from open to close with the long shadows indicating both bulls and bears were active during the session. These long shadows show high price fluctuation within the period the candlestick represents despite the closing price being so near the opening price. After a long bullish or bearish trend a spinning top can show a potential change in direction either temporarily or ongoing.

A doji is another key candlestick that even analysed separately of the trend can tell you a lot of information about the markets. A doji forms when the opening price is virtually equal to the closing price giving a very thin body making the overall candlestick looking like a cross. Although an ideal doji looks has the shadows a similar length, a less robust doji can also be used to understand a market trend. If one shadow is longer than another then this could indicate that the bulls or bears might be getting their way, despite the close price not changing from the open price. You may wonder who decides how close the opening and closing price has to be to count as a doji? Well different assets have a different metric for determining the robustness of the doji depending on price, recent volatility and comparing it to recent candlesticks.

To analyse the market trend you should identify a doji within a trend, judging its position compared to the preceding candlesticks. After a long green candlestick a doji indicates buying pressure has dropped and shows a change in the trend is going to happen soon. The same applies for opposite forces where a trend of red candlesticks is followed by a doji signaling the selling pressure has weakened. A doji after an uptrend is more significant as buying pressure is required to maintain an increase in price whereas the price can fall without an increased selling pressure simply if there is a lack of buyers. Spotting a doji isn’t enough information to signal a reversal in the trend so look out for other patterns to confirm what the doji indicates. To confirm a directional change, look for a long red candlestick lower than the green candlestick.

Long-legged doji have long upper and lower shadows that are roughly equal in length. This demonstrates there is high indecision in the market as long shadows present prices traded much above and below the opening and closing price.

There are a further two types of doji that deserve special recognition. Dragonfly doji look like a capital “T” with a long stem or using the descriptors of candlesticks, no upper shadow, a long lower shadow and almost no body. This can be seen when sellers are strongly present during the trading session attempting to push down the price yet over that timeframe not achieving a move in price. A dragonfly doji can be significant after a long downtrend or at a support level to indicate a bullish reversal. Similarly after a long uptrend or at the resistance line, the presence of this doji could signify a potential bearish reversal. The opposite of a dragonfly doji is a gravestone doji which looks like an upside down “T” with a long top shadow and almost no bottom shadow. The presence of this doji indicates that buyers are more dominant pushing up prices over the session yet failing to push the closing price higher than the closing price. After a downtrend, long red candlestick or at a support line the presence of a gravestone doji indicates some buyers are active and could lead to a bullish reversal. The opposite also applies.

Candlesticks demonstrate the fight between bulls and bears or buyers and sellers. The bottom of the candlestick if the close is close to the high represents a win for the bears and the top represents a win for the bulls the closer the close is to the low. As mentioned before if there is a long green candlestick then bulls are in control with a shorter body demonstrating a weaker advantage. The reverse is also true when a long red candlestick is present. When there is a struggle you can see doji forming, with the longer the upper shadow showing bulls are more active and if the lower shadow is longer than bears are creating more pressure.

Candlestick Positions

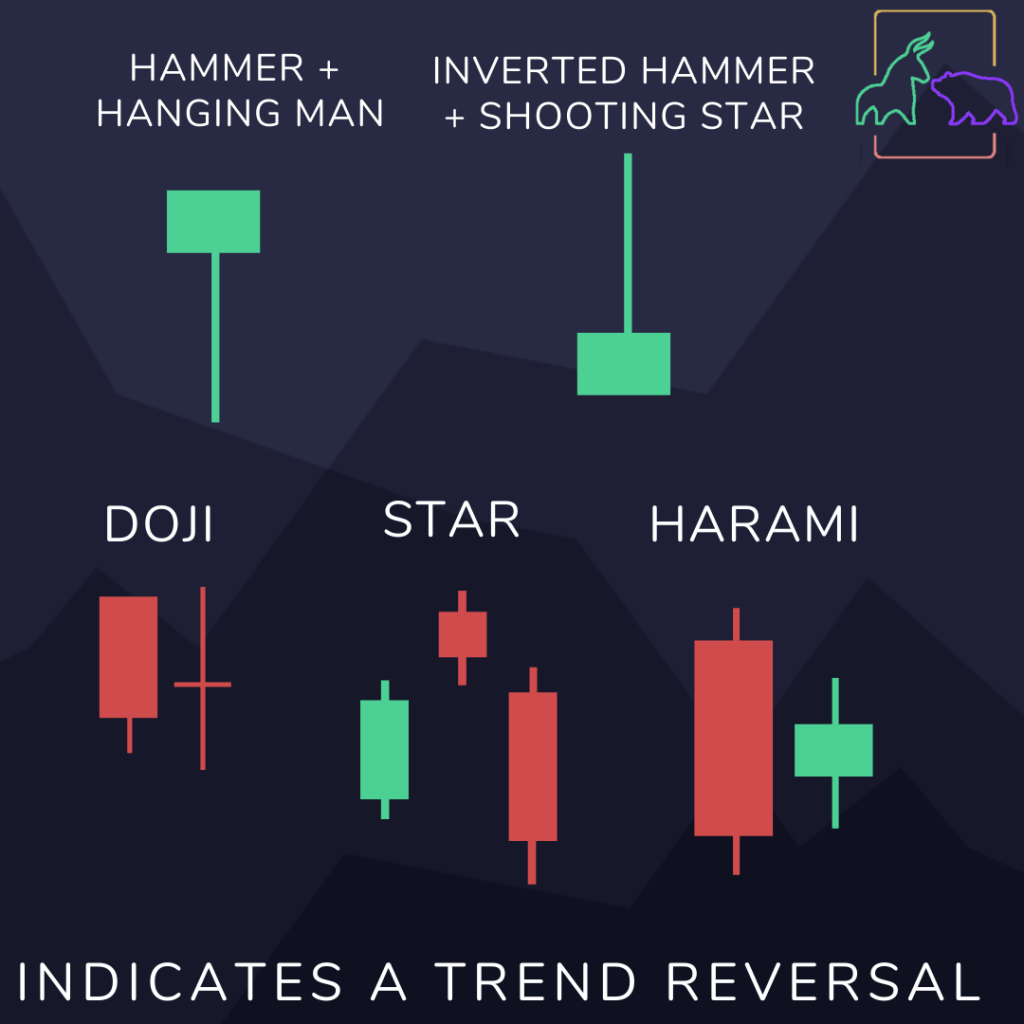

A star position is a candlestick that does not overlap with the previous candlestick and usually has a small body compared to the previous candlestick. The star appears isolating from the previous candlestick and can be above or below. Other special candlesticks like doji, hammers, shooting stars and spinning tops can feature in as a star position candlestick.

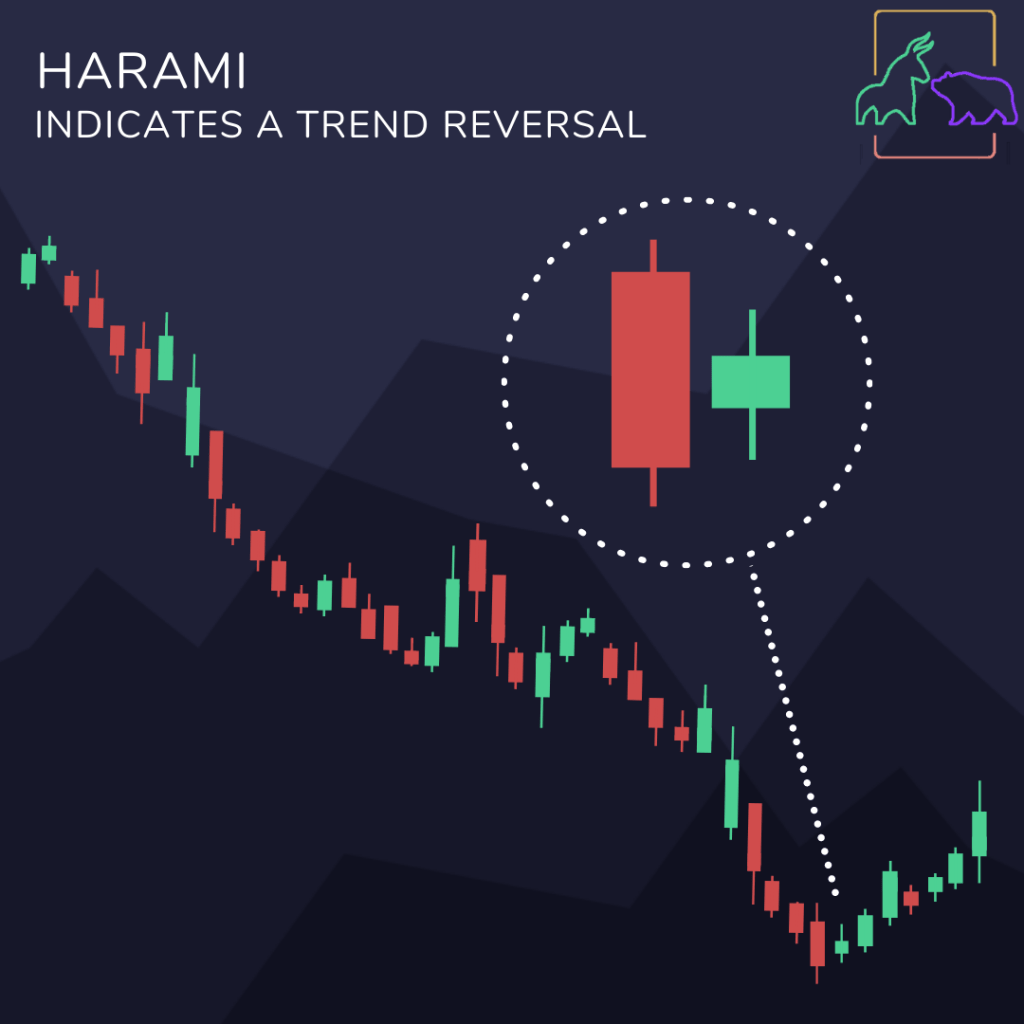

Similar to a candlestick position is a Harami position which has a long candlestick followed by a very short one. The word itself means pregnant in Japanese which makes this position easy to remember as the larger candle holds the little candle within it. After a long candlestick a short candlestick of the opposite pressure is present and should fit within the body of the larger candlestick, say a long green candlestick is followed by a short red candlestick.

Long shadow reversals

There are two pairs of candlestick reversal patterns which are made from a singlestick with a small body, one long shadow which is about double the length of the body and one very short shadow. One pair consists of the Hammer and the Hanging Man which are identical candlesticks with short bodies and long lower shadows whereas the second pair, the Shooting Star and Inverted Hammer have identical candlesticks but with small bodies and long upper shadows. The former pair mentioned appear after a long decline whereas the latter pair mentioned form after an upward trend.

The Hammer and the Hanging Man look the same but mean different things depending on the candlestick patterns that come beforehand. The Hammer indicates a bullish reversal after a decline or a support line. The long lower shadow demonstrates that sellers acted to drive down prices during the session before buyers took over to close the session. Although this seems like a clear indication of a reversal you should watch out for other signs to confirm this. For example, a gap up where there is no overlap between bodies of the current and previous candlestick or a long green candlestick. The opposite is the Hanging Man which can mark the turn to a bearish trend or the resistance line. Like the Hammer, you must look for confirmation in the form of a gap down or long red candlestick.

The Inverted Hammer and Shooting Star look the same yet depend on the surrounding candlesticks to present a full understanding of a change in the trend. Both candlesticks have small bodies, long upper shadows and very small lower shadows to make a trend reversal. The Shooting Star forms after an advance in the star position to mark a trend reversal or resistance line. These reversal candlesticks can be confirmed by a gap up or down or a long candlestick that follows. The Inverted Hammer looks the same yet forms after a decline or downtrend. The long wick shows a strong buying pressure was present during the session but couldn’t overcome the selling pressure. The bulls failed for a reason so look for confirmation before making a decision on it.

Before you invest with your new knowledge, you will need to open an account with a broker to manage your investments.

Choosing the best online stock broker can make the difference from an easy and exciting new experience to constant frustration and disappointment. Accessing financial markets through online brokers is easy and inexpensive but there are so many out there tailored to a different sort of customer so choose the right broker that will optimise your user experience and profits.

If you’re just starting out we recommend eToro and easyMarkets for their easy to use interfaces and fee – free trading.

Now you know the most common candlestick charts you can get started with trading! We recommend eToro and easyMarkets for beginners.

After the announcement of Beyond Meat Inc (BYND) earnings report and strategic partnerships with McDonald’s and Yum! the stock has closed at a loss on Thursday. What does the future look like for the plant based burger company?

Beyond Meat Inc (NASDAQ: BYND) saw its share price close 5.5% lower after it reported high Q4 2020 losses. The company saw a Q4 net loss of US$25.1 million, compared to US$0.5 million in the prior year period.

In the fourth quarter of 2020, net loss included US$3.7 million specifically related to COVID-19, including inventory write-offs. Excluding these items, the adjusted net loss was US$21.4 million in the fourth quarter of 2020.

Beyond Meat and McDonald’s have signed a three-year global strategic agreement. This means Beyond Meat will supply the McPlant burger, a new plant-based burger being tested in some McDonald’s markets globally. They will also collaborate on co-developing other plant-based options for McDonald’s.

Beyond Meat have also partnered with Yum! The company will supply large restaurant chains such as KFC, Pizza Hut and Taco Bell over the next several years.

Beyond Meat’s shares were up as much as 53% earlier this year, after the stock hit a year-to-date peak price of US$192 on 27 January. The rally came after PepsiCo and Beyond Meat announced plans to form The PLANeT Partnership, LLC (TPP), a joint venture to develop plant-based products.

Beyond Meat shares are still up some 14.5% year-to-date. In the last year, the alternative food manufacturer’s share price has skyrocketed over 77%, as the Covid-19 pandemic boosted the company’s retail sales in the first and second quarters of 2020.

Before you invest with your new knowledge, you will need to open an account with a broker to manage your investments.

Choosing the best online stock broker can make the difference from an easy and exciting new experience to constant frustration and disappointment. Accessing financial markets through online brokers is easy and inexpensive but there are so many out there tailored to a different sort of customer so choose the right broker that will optimise your user experience and profits.

If you’re just starting out we recommend eToro and easyMarkets for their easy to use interfaces and fee – free trading.

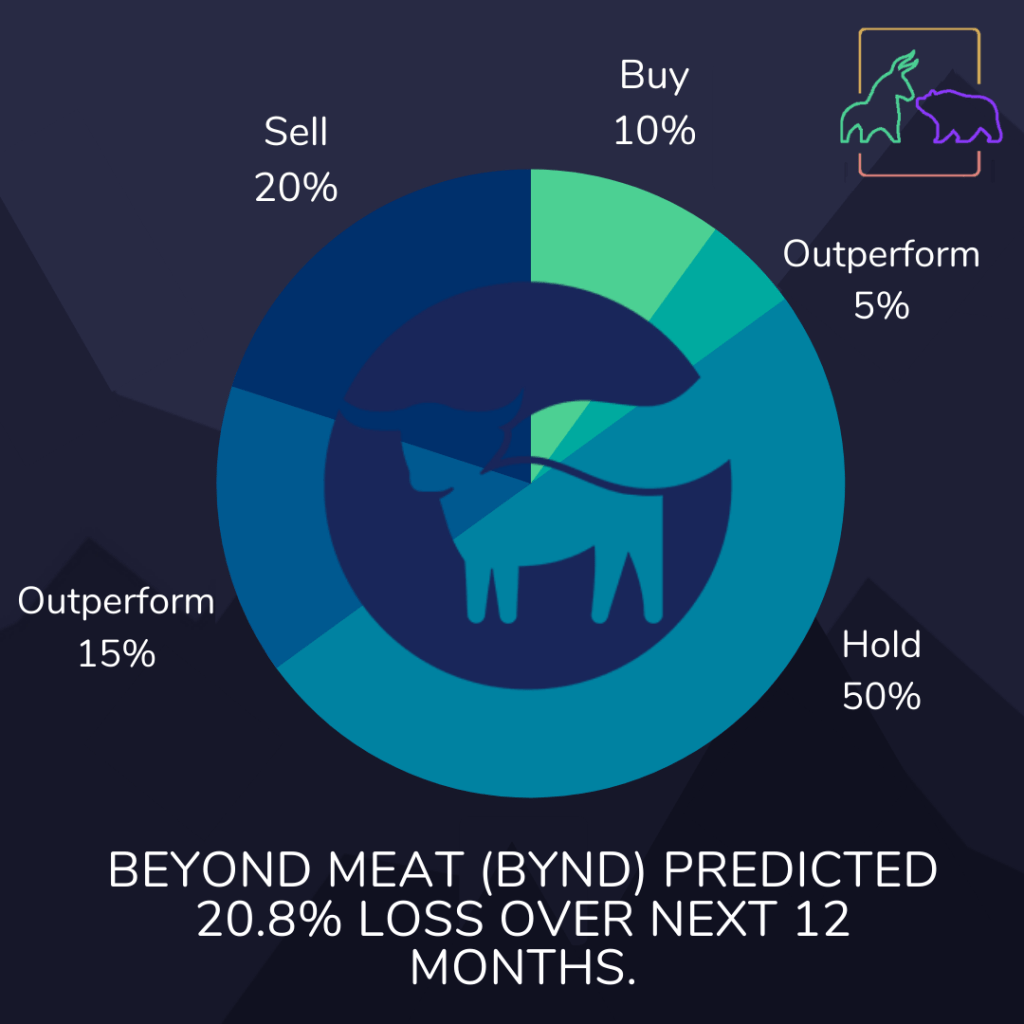

The stock has received a consensus rating of ‘hold’ and an average price target of US$115.68 from 20 analysts, according to the latest MarketBeat data.

Analysts see a 19.5% downside on the stock in the next 12 months.

Beyond Meat posted an adjusted net loss of US$0.34 per common share, which is bigger than analysts’ projections of US$0.14.

Beyond Meat have not proven much resilience over the pandemic resulting in a massive loss of earnings which has no doubt affected the stocks price forecast. With vegetarianism on the rise and with a new deal with food giants, will beyond meat make a strong come back over the longer term? If you are ready to invest, we recommend eToro and easyMarkets for beginners.

Candlestick patterns are a really useful way to work out when trend reversals will happen so you can time entry and exit points. If you want to start trading, reading candlestick patterns are essential!

Technical analysis was first used by the Japanese to trade rice back in the 17th century.

Technical analysis is guided by some essential principles:

Understanding the price action is more important than what guides the price as information is fundamentally reflected in the price

Traders move markets based on expectations and emotions

Markets fluctuate

The market price may not reflect the underlying value of an asset.

Candlestick charting was first used around the 1850’s and was developed by a rice trader called Homma. SInce then candlestick charting has evolved to the more complex form we use today to trade better.

What does a candlestick show?

Candlestick charts use the data for opening, high, low and closing values for each time period you want to display. The body of the candlestick is the middle section and can be hollow or filled. The thin lines above are wicks and below are tails – these shadows represent the high and low range of data. If a stock closes higher than it opened then the body is hollow or filed in green and the top of the body shows the closing price and the bottom of the body reflects the opening price. Whereas if the stock price fell over the period then a filled body or red body is drawn with the top of the body representing the opening price and bottom representing the closing price.

Each candlestick has four data points:

Open: The opening price

High: The highest price over a fixed period

Low: The lowest price over a fixed period

Close: The closing price

Candlestick charts are the preferred chart of choice for traders as they are visually appealing and easy to interpret. Each individual candle summarises price action showing whether the price has risen or fallen and gives an idea of the spread.

A bullish candlestick is green or hollow and has the open BELOW the close indicating a buying pressure

A bearish candlestick is red or filled and has the open ABOVE the close to show a selling pressure.

What makes each one different?

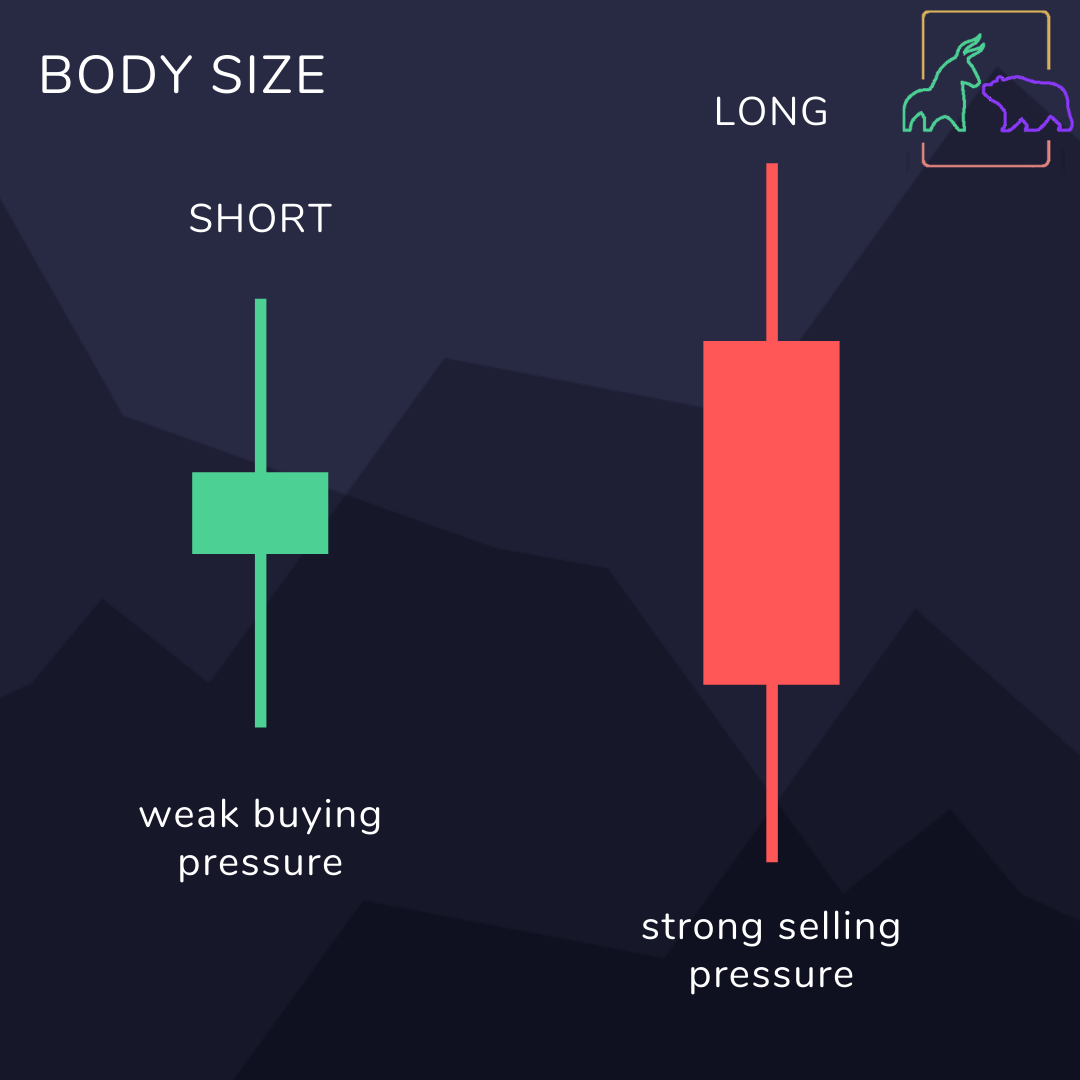

Body size: The length of the body explains how much pressure there is to push the price in one direction. A longer body means there is a more intense buying of selling pressure. Let’s say you see a long red or filled candlestick, this means the open is far higher than the close price. This suggests the price dropped quickly and sellers were aggressive over the period. Although the individual candle reflects a bearish market, remember this is part of a series of candlesticks and it is looking at patterns across a number of candlesticks which gives you the best indication of how the market is moving. The same principle applies if it was a bullish candle. A run of long bearish candles can mark a turning point or resistance level as an extended period of aggressive selling can overdo it and push the market into a reversal where buying becomes more dominant – switching from a run of red candlesticks to green candlesticks.

Shadow Length: The upper shadows represent the session high and the lower shadows show the session low. Candlesticks with short shadows indicate trading action is near to the opening and closing price whereas long shadows show the prices deviate far from the opening and closing prices.

But what happens when the upper and lower shadows are different lengths? A candlestick that has a long upper shadow and a short lower shadow indicates that buyers are putting the most pressure on the period the candlestick reflects, with more buyers, bidding pushes prices even higher but overall sellers force down prices. Whereas candlesticks with long lower shadows and short upper shadows indicate sellers dominate driving prices down before buyers bid prices higher – this strong close creates the long tail.

Candlesticks are great for showing you the relationship between the opening and closing price however there are a few omissions. Simplifying price action over a certain time frame is great when you want to step back and analyse the larger trend. Remember you can always change your timeframe to see a more in depth look at the price data.

A candlestick shows the extremes of the trading session and the opening and closing price yet this cannot show the change within the time period for example if the high was before or after the low. Although it seems fairly insignificant, its subtleties of change can present the volatility of that particular asset at that particular time. The difference between a strong bullish presence and a switch between bullish and bearish dominance before bulls coming out on top indicates how strong the trend will be.

Before you invest with your new knowledge, you will need to open an account with a broker to manage your investments.

Choosing the best online stock broker can make the difference from an easy and exciting new experience to constant frustration and disappointment. Accessing financial markets through online brokers is easy and inexpensive but there are so many out there tailored to a different sort of customer so choose the right broker that will optimise your user experience and profits.

If you’re just starting out we recommend eToro and easyMarkets for their easy to use interfaces and fee – free trading.

Now you know the basics on how to read candlestick charts you can get started with trading! We recommend eToro and easyMarkets for beginners.

This week saw a massive dip in the stock market, but Twilio fared well. This high-growth company delivering cloud-based communications rose almost 8% yesterday. The company’s 65% year-on-year growth begs the question, is Twilio a buy?

The stock market crashed yesterday due to a mix of economic uncertainty around vaccine rollout and announcement of jobless claims in the US. .Amid the sea of red on Wall Street, Twilio climbed higher. The cloud-based communications specialist reported fourth-quarter financial results that confirm the stock is growing fast.

Twilio, Inc. (TWLO) engages in the development of communications software, cloud-based platform, and services. Revenue for the fourth quarter jumped 65% year-on-year, capping a year of 55% top-line growth for the company. Dollar-based net expansion rates of 139% for the fourth quarter and 137% for 2020 demonstrates customers are feeding more and more back into the business. The company now has over 221,000 active customer accounts, up 42,000 from a year ago.

Twilio also expects the good times to continue. It projected guidance for first-quarter sales to grow between 44% and 47%. That might seem like a slowdown, but Twilio has historically been quite conservative in its guidance.

Chart from money CNN

Twilio expects their high growth to continue with projections of Q1 sales up 44 – 47%. Considering Twilio have a history of estimating conservatively, this target will be easily achieved. As developers implement new operational standards, Twilio makes their life easier. More than 10 million developers around the world are using Twilio’s library of software to embed new means of communication within applications. Twilio’s popularity was proven with a 65% increase in revenue year-on-year (December 2020) equating to $548 million.

“Twilio’s 65% year-over-year total revenue growth in the fourth quarter continued the strength and momentum we saw throughout an outstanding year of results in which we delivered $1.76 billion in revenue,”

– CEO Jeff Lawson

“These results reinforced that we are addressing a generational opportunity, and with our acquisition of Segment and strong traction with Flex, we are building the leading customer engagement platform to improve every interaction that businesses have with their customers.”

– CEO Jeff Lawson

The Covid-19 disruption has helped Twilio grow in new areas, including telehealth and online education. Whereas, its pandemic-hit dining and ride-sharing markets are only just starting to improve. A diversified customer base has helped Twilio during the pandemic, investing more in back-office processes, sales and marketing to target new opportunities.

Last year, Twilio announced they would acquire Segment, costing $3.2 billion in stock. The move to add a customer data business will set Twilio ahead of other competing platforms. Although new integrated products are yet to be announced.

Before you invest in Twilio, you will need to open an account with a broker to manage your investments.

Choosing the best online stock broker can make the difference from an easy and exciting new experience to constant frustration and disappointment. Accessing financial markets through online brokers is easy and inexpensive but there are so many out there tailored to a different sort of customer so choose the right broker that will optimise your user experience and profits.

If you’re just starting out we recommend eToro and easyMarkets for their easy to use interfaces and fee – free trading.

Should I buy or sell Twilio?

Overall, Twilio’s strong performance and high growth potential means it is a BUY.

Chart from money CNN

Technicals show us the stock is well worth investing in with a relative strength line that has risen to record highs. A rising RS line means TWLO stock is outperforming the S&P 500 index.Overall, Twilio rates highly on both key fundamental and technical metrics.

Price Forecast

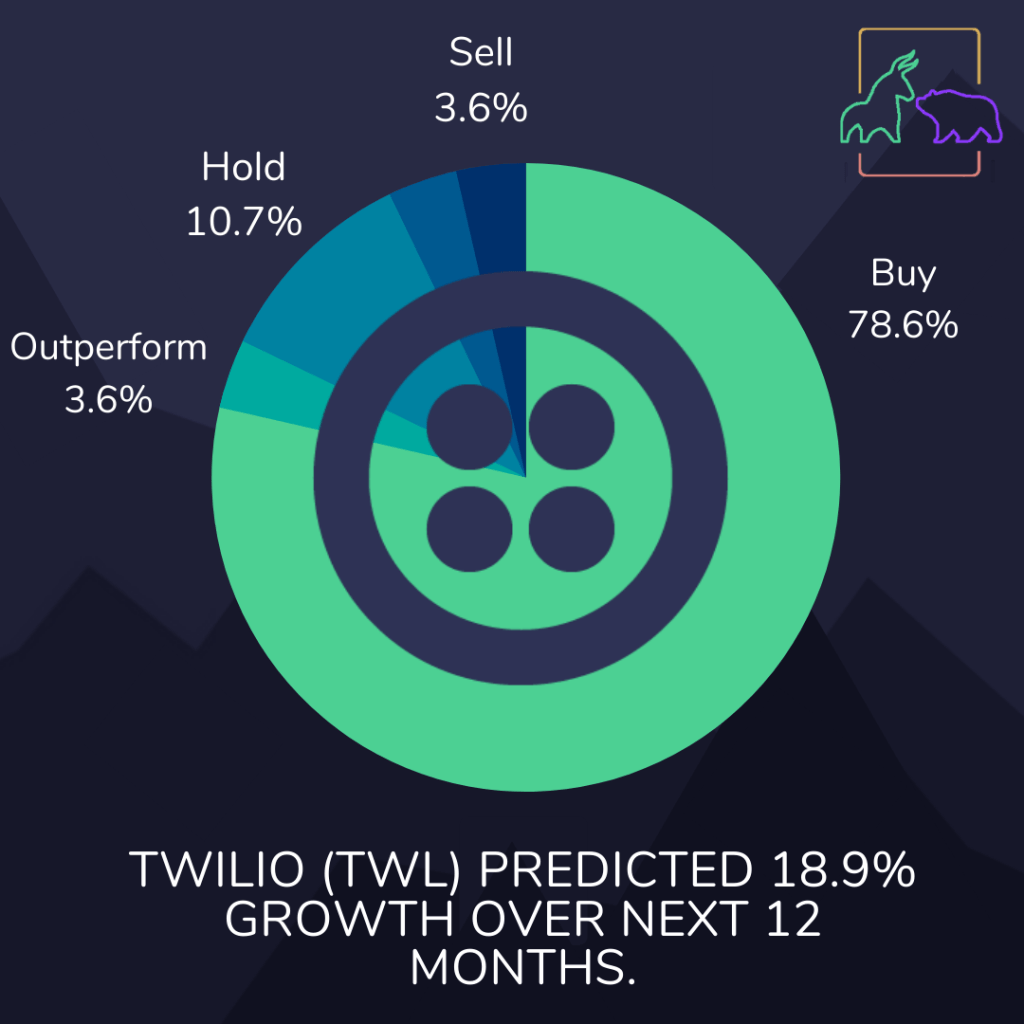

Outlook for the first quarter sees a revenue of $526 – $536 million, well above the $487.2 million in sales analysts predicted. The median estimate after 12-months is a staggering 18.9%. But once Q1 performance is released, we can expect a positive adjustment.

Twilio’s strong performance and high growth potential proves it is a strong buy. Want to start investing? We recommend eToro and easyMarkets for beginners.

With the stamp duty holiday almost over and the third lockdown likely to end there is going to be some big movement in the housing market. There are some great ways to invest in the property market indirectly. Read on to get started!

Housing Market Update

Not surprisingly there has been some changes to supply and demand of houses due to the pandemic. The highest demand change has been for properties in outer London as buyers are preferring space over location. It appears homeschooling and cold weather conditions are encouraging many people to hold off selling homes until spring, accentuating the usual seasonal trend. After three months of falling house prices in London, there has been a 3% increase in property prices from January to February. Overall, however, the average asking price for London properties has fallen by 1.1% this February compared to February 2020.

The stamp duty holiday is soon to end leading to predictions that buyer demand will decrease as the lengthy buying process will mean missing the deadline to save up to £15,000. The stamp duty cuts have promoted a sense of urgency in the housing market, the average time to agree a sale at 57 days compared to 71 days for the previous year.

Overall, the number of new buyers has increased, despite few being able to take advantage of stamp duty cuts. With demand overpowering supply, prices are being pushed up. A massive 21% drop in sellers is likely a result of families delaying selling due to homeschooling pressures. Last year set the precedent of seeing more buyers moving to properties more suited to lockdown needs.

As property markets are open across the UK with estate agents allowing in person moving and no restrictions on moving, the market has been on the rise. Property sales in December are up 32% year-on-year based on transactions statistics from HMRC. Rightmove found asking prices had dropped 0.9% month-on-month in January but risen 3.3% year-on-year.

Housing Market Predictions

With government coronavirus financial support schemes and stamp duty cuts coming to an end it is unsure whether the increased activity in the housing market will continue. The current best guess is that house prices will level off in 2021. Rightmove predicted house prices will rise 4% over 2021 following a lull in Q2 after stamp duty cuts end. Whereas Halifax forecast house prices to fall by 2 – 5% this year and the Centre for Economics and Business Research (CEBR) predicted a fall by 5%. Estate agents Savills and Hamptons are holding strong that house prices will stay the same, whereas Chestertons and Knight Frank predict a 1.5% and 1% rise respectively. If you think this is confusing, don’t worry we agree! Therefore unless you were planning to buy or sell anyway it is best to stay clear of investing in the house market until trends are clearer.

The biggest tell on how house prices will perform is the state of the economy. If there is a sharp decline in the economy accompanied by a surge in unemployment then we are likely to see ‘pressure sales’. People who can no longer keep up mortgage repayments have no option but to sell their homes, and quickly. Although this crash is more than possible, support from the government and banks will more than likely prevent forced sales.

Before you invest in property stocks, you will need to open an account with a broker to manage your investments.

Choosing the best online stock broker can make the difference from an easy and exciting new experience to constant frustration and disappointment. Accessing financial markets through online brokers is easy and inexpensive but there are so many out there tailored to a different sort of customer so choose the right broker that will optimise your user experience and profits.

If you’re just starting out we recommend eToro and easyMarkets for their easy to use interfaces and fee – free trading.

How to invest in property indirectly

Investing in the housing market indirectly could be very lucrative and significantly easier than investing directly.

Real estate investment groups (REIGs) are great for people who want to own real estate but without the hassle. A REIT is created when a corporation (or trust) uses investors’ money to purchase and operate income properties. Like regular dividend-paying stocks, REITs are a solid investment for stock market investors who want to have a regular income.

British Land (LSE: BLND) is listed on the FTSE 100 and is a huge commercial property REIT. This £5.5bn firm owns an £11.7bn portfolio of property. This company offers a 5.3% dividend yield and currently is undervalued.

Big Yellow Group (LSE: BYG) is a FTSE 250 stock option, the company provides storage units and holds A LOT of property. The Big Yellow share price has doubled over the last five years as the business has grown rapidly.

Berkeley Group Holdings (LSE: BKG) is an upmarket homebuilder. This FTSE 100 firm focuses on London and the south east. Berkeley shares have performed strongly this year pushing the company to return £280m to shareholders each year until September 2025. Shares offer a cash-backed yield of 4.4%.

Now we’ve provided our top housing stock options, will you be investing? We recommend eToro and easyMarkets for beginners.

Bumble shares open at $76, $33 above the IPO price. Is it a good time to buy shares in this dating app?

Shares in the dating app Bumble (BMBL) have risen 76% on their stock market entry, resulting in a valuation of £10 billion. Massive first-day trading gains are to cause a rumble with venture capitalists who argue the initial offering was under priced.

The IPO was led by Goldman Sachs Group Inc., Citigroup Inc., Morgan Stanley and JPMorgan Chase & Co. Bumble’s shares began trading on Thursday on the Nasdaq Global Select Market under the symbol BMBL.

Bumbles History

The Texas based company was founded in 2014 by Whitney Wolf Herd, a cofounder of the rival dating app, TInder. She sued Tinder after an alleged sexual harassment case and left the company promptly after in the same year. She received a $1 million settlement from Tinder’s parent company Match Group.

Later, in 2018, Match had filed a lawsuit against Bumble for intellectual property infringement which sparked Bumble to take out a counter-lawsuit accusing Match of fraud and theft of trade secrets. Both lawsuits were subsequently dropped.

Bumble is different to other dating apps centuring on women to make the first move. Though bumble has subsequently added features to meet new friends (Bumble BFF) and business contacts (Bumble Biz). The company has around 54 million monthly users, showing clear competition to Tinder which has 100 million users per month.

With the pandemic going on, the online dating market has boomed as people seek alternatives to in-person dating. However, Bumble published a net loss of $84 million between February and September last year. This poses a huge question to the world of online dating, will people continue to use these services post-pandemic?

Recently, there have been several companies that have surged after their debut on the stock market. Food-delivery company DoorDash rose 86% and Airbnb more than doubled after opening on stock markets. 2020 saw first-day rallies triple the average over the past 40 years.

Before you invest in Bumble, you will need to open an account with a broker to manage your investments.

Choosing the best online stock broker can make the difference from an easy and exciting new experience to constant frustration and disappointment. Accessing financial markets through online brokers is easy and inexpensive but there are so many out there tailored to a different sort of customer so choose the right broker that will optimise your user experience and profits.

If you’re just starting out we recommend eToro and easyMarkets for their easy to use interfaces and fee – free trading.

Should I buy?

With Bumble’s IPO price at $43 there is plenty of room for growth. Sales are predicted to expand by 20% to 2023 with a 12-13x forward sales multiple that beats TInder. But it is uncertain whether there will be as much public interest in the premium service when in-person dating picks up again post-pandemic. Market research indicates that people will adopt the new normal of online dating making it likely that most (although not all) of the business these dating apps have acquired over the pandemic will continue.

Bumble offers a competitive advantage over other dating apps with their women first approach.

“They made the successful bet that where women are, the men will follow. And women will go where they feel comfortable and empowered,”

– Jeremy Abelson, founder of Irving Investors, who supported the IPO.

Bumble also offers services beyond dating. Bumble BFF, the friend-making part of the app, only has 9% of Bumbles total users. Competitor Ablo, owned by the Match Group has seen a continued interest in finding friends virtually so there is definitely potential to grow.

It is often thought that investing in IPOs is risky. Lyft shares become public a few years back yet still haven’t reached the price of their IPO two years later. It is also important to consider that IPO investing favours institutional investors as these organizations are able to acquire shares before the retail market opens, giving them a distinct advantage to retail investors.

Furthermore, the digital dating sector has high competition and with Match Group forecasting a revenue below what analysts expected, the potential for growth from the new kid on the block is somewhat limited.

Normally, we would look at the stocks recent performance to judge whether it is a good stock to buy, but with Bumble trading for less than 24 hours, it’s best not to rely on this indicator!

There are currently no published analyst ratings for Bumble so it could be a big risk to buy now.

As Bumble enters the market everyone is wondering if their IPO was undervalued. Will we see BMBL’s share price rise? Will you be investing? We recommend eToro and easyMarkets for beginners.

Why trade penny stocks? They’re cheap! To meet the criteria of being a penny stock, they have to be listed at less than $5, meaning you don’t need a lot of capital to start investing. The potential for large returns also makes penny stocks attractive to investors.

What are Penny Stocks?

A penny stock is a stock of a small company that trades for < $5 per share, as defined by the Securities Exchange Commission (SEC). These companies are typically relatively new so don’t have a long performance record and have a small market capitalisation making them speculative investments. Most penny stocks are not always available on large exchanges like the New York Stock Exchange (NYSE), so are mainly traded via over-the-counter (OTC) transactions.

As penny stocks are tied to small companies and are traded less frequently than most stocks they have a lack of liquidity as there is less demand for them in the markets. This means prices may not accurately reflect the market, a similar issue that some alternative investments find. Their lack of liquidity means penny stocks are considered highly speculative. Being highly speculative means both there is a high potential for profit but also a high risk of losing money with this type of investment.

As there is a higher risk associated with penny stocks than typical stocks it is advised that you set a stop-loss order and fully understand the price you want to enter and exit the trade at. Penny stocks are high-risk investments, so while it is possible to benefit from explosive gains there is also the potential for you to lose money.

Penny stocks are provided by small businesses as a way to get funding, usually for companies just starting out. They sell stocks at low prices and at a much lower quantity than typical stocks or blue-chip stocks. Blue-chip companies are typically well-established and financially sound as opposed to small companies that come with high financial risk.

There are a few reasons why penny stocks are risky:

Private records mean the public have a lack of information to use to consider buying penny stocks. Unlike blue-chip stocks, penny stocks are not required to file financial statements with the SEC – who regulate markets.

No minimum standards means penny stocks can be listed on OTC exchanges no matter their performance. Needless to say this makes investing in penny stocks risky.

Low liquidity is inherent to penny stocks as they are not traded frequently. This opens up the opportunity of fraud as traders can manipulate prices in a pump and dump.

OTC Penny Stocks v major exchange Penny Stocks

Some penny stocks are listed on major market exchanges if they are large, but based on market capitalisation trade at < $5 per share.

Ever heard of Pink Sheets? These are the cheapest of all publicly traded stocks and are traded on the OTC market. The OTC market does not require them to comply with the safety measures and regulations that stocks listed on large echanges such as NYSE or NASDAQ require. To trade on these larger exchanges the company must present their financial history and their stock must consistently trade at above $1 per share. A company unwilling to be transparent about their finances raises a huge red flag, therefore it may be best to avoid trading OTC penny stocks. Trading on OTC markets not only has a lack of regulation but also typically has stocks with less liquidity, making them more dangerous to trade.

We pose that investing in penny stocks listed on larger exchanges will reduce your risk a little. Penny stocks listed on larger exchanges are cheap but still provide the high potential for gains without the risk of fraud or bankruptcy.

How to choose the best Penny Stocks?

You are fundamentally looking to invest in penny stocks that are likely to make big moves.

To find specific stocks to trade you can look for certain criteria:

News presence that will likely catalyse the stock. This can be anything from earnings reports to the release of a new product.

Float volume under 100 million shares as this means the stock price is more open to buying pressure that can push the shares up quickly.

High relative volume so you know you can get rid of the stock if you want. Check pre-market volumes to ensure you have plenty of liquidity.

Before you invest in penny stocks, you will need to open an account with a broker to manage your investments.

Choosing the best online stock broker can make the difference from an easy and exciting new experience to constant frustration and disappointment. Accessing financial markets through online brokers is easy and inexpensive but there are so many out there tailored to a different sort of customer so choose the right broker that will optimise your user experience and profits.

If you’re just starting out we recommend eToro and easyMarkets for their easy to use interfaces and fee – free trading.

Top Penny Stocks

Zomedica (ZOM) are in the veterinary industry and have developed a product called Truforma which has gained a lot of interest. The stock will pick up speed accordingly so get in there quick. Currently trading at $1.90 per share.

Cerebain Biotech (CBBT) develops ground-breaking treatments for Alzheimers, a condition that is becoming more and more prevalent. They have an upcoming merger with PKG which will likely push the stock high. Currently trading at $0.20 per share.

ToughBuilt Industries, Inc. (TBLT) have been rising fast with sales increasing 30% over just five years. After a recent rise, we may see a dip soon – presenting a good opportunity to buy. Currently trading at $1.50 per share.

Gold Resource Corporation (GORO) works in gold and silver production. Due to recent uncertainty with the gold market, this penny stock is an absolute bargain at just $3.00 per share. With commodity prices set to rise over 2021, this may be a great opportunity for profit compared to larger gold companies on the market.

Arcadia Biosciences, Inc. (RKDA) manufactures and sells agricultural chemicals and technologies. Stock prices dropped sharply after a direct offering scared investors into a sell-off with fears that the company may be on the brink of dilution. If the stock rises past $3.50 (currently at $3.20) then the rise should continue through 2021.

Now you know that penny stocks can get you high potential gains but high potential losses. Will you be investing? We recommend eToro and easyMarkets for beginners.