ISA’s are great as they have tax benefits and are really simple to use. Thanks to the UK government, people can build up large tax-efficient sums to make their money work harder.

Individual Savings Accounts (ISAs) are open to UK residents to save and invest in a tax-efficient way. Holding investments in an ISA avoids capital gains tax and further income tax. We all want to know how we can invest our cash to get the best interest rates and incentives, so read on to find out more.

Each year you can invest up to £20,000 in ISAs, this means you can put it all in one or split it between various types.Make the most of your money by putting it in the best-paying savings vehicle possible, and when that is maxed out, turn to the next best option.

How to choose the best type of ISA for you

It is important to compare different types of ISA to maximise your returns and allow you to access your money as you need. Note you can invest your annual ISA allowance into one type of ISA, or split it across a combination of products upto the value of £20,000 a year.

Consider the following when making your decision:

- What level of risk are you comfortable with?

- What are you saving for?

- How long will you save or invest for?

- What is the most efficient method of saving for your goals?

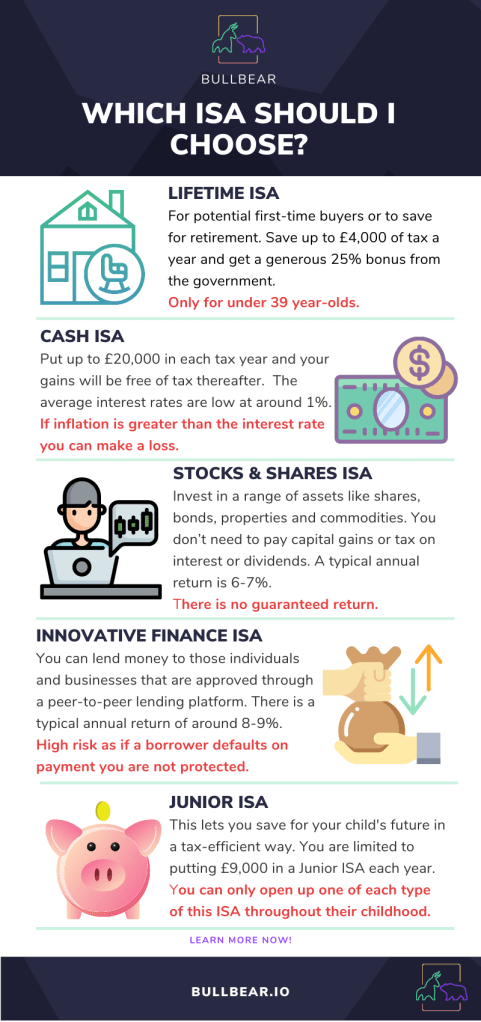

Lifetime ISA

Lifetime ISAs can be utilized by potential first-time buyers or to save for retirement. Anyone aged 18 – 39 can open a LISA and save up to £4,000 of tax a year and get a generous 25% bonus from the government on top! If you made the most of this type of ISA by saving the max £4,000, you will actually have £5,000. Then when you want to buy your first home you can use your accrued money towards a deposit of a property of up to £450,000 or for your retirement.

Sounds too good to be true right? Many people are often capped fairly early on in their savings career. Also, it is capped at entering an initial sum of £1,000 and then £200 a month. Another thing you may want to consider is if your first property is likely to be less than £450,000, while for most parts of the UK this wouldn’t cross your mind, but if you live in a big city and are looking for a sizable or central location property, it is definitely worth a few minutes to consider.

Does this sound familiar? Well the Help to Buy ISA aimed at first-time buyers is a similar set-up, although they are being phased out by the government so you can no longer apply for one of these.

Cash ISA

A Cash ISA works similarly to a traditional savings account, as it lets you save money and pays you interest. The difference is that a Cash ISA doesn’t tax your interest.

There are two main types of cash ISA. A fixed-rate cash ISA is essentially a savings account where the interest isn’t taxed and the interest is a fixed number and requires your cash to be tied up for a certain number of years (usually 5). If you are over 16 you can put up to £20,000 in each tax year and your gains will be free of tax thereafter. Whereas, an easy-cash access ISA doesn’t have withdrawal restrictions, freeing up your cash to be withdrawn whenever you like.

The average interest rates on Cash ISAs are only around 1%, so you could get better returns elsewhere.

The biggest thing to watch out for is checking inflation doesn’t outpace the interest rate of your Cash ISA, as this would produce a small loss. If your aim is to grow your savings then this is something to 100% avoid.

Stocks and Shares ISA

Here you can make the most of your £20,000 tax-free ISA allowance with a potentially higher rate of return than other types of ISA. A Stocks and Shares ISA is fundamentally an investment ISA as your money is invested in a range of assets like shares, bonds, properties and commodities. Again, you don’t need to pay capital gains you make on interest or dividends so is a great way to get involved with investing tax-free.

There are a range of plans out there which range from low to high risk (although they are all fairly safe). If you invested an initial sum of £5,000 and then £200 each month for 5 years your investment could grow to almost £22,000 on an 8% annual growth rate. The stock market is volatile in the short-term, but tends to outperform cash in the long-term, so most financial advisors recommend investing for at least five years.

A typical annual return is 6-7% , although returns can go down as can they go up. It is worthy to note this ISA might not be all that beneficial as you can already earn tax-free capital gains up to the Annual Exempt Amount of £12,300 and a Dividend Allowance of £2,000. So it is only worth opening up a Stocks and Shares ISA if you exceed these allowances.

You should be aware of the risk with a Stocks and Shares ISA that there is no guaranteed return and there is the possibility that the value of your investments could go down. When comparing the higher returns of a Stocks and Shares ISA to a Cash ISA, it may be worth it. To mitigate some risk you can invest over the long-term as this typically smooths the ups and downs of the market and allows your money to compound. Note also there are fees associated with this sort of ISA.

Innovative Finance ISA

This lesser known ISA type allows you to lend money to those individuals and businesses that are approved through a peer-to-peer lending platform. This gets you a return of a fixed amount of interest which is not taxable.

This type of ISA can get you an annual return of around 8-9% but the risks are much greater than other types of ISA.

This direct lender-borrower scheme brings greater risks as borrowers can default on payments which are unable to be compensated by the Financial Services Compensation Scheme.

Junior ISA

Junior ISAs allow you to save for your child’s future in a tax-efficient way. You can open a Junior ISA for your child anytime before they are 18 and as long as they don’t have a Child Trust Fund. You are limited to putting £9,000 in a Junior ISA each year and have the option of putting your money in a Junior Cash ISA or a Junior Stocks and Shares ISA (or both!).

Something to remember though is your child owns the ISA, meaning they are able to withdraw money when they turn 18. However if they leave the money in the ISA it is converted to an adult ISA to continue saving. Note you can only open up one of each type throughout their childhood instead of the one per year that is allowed for adult ISAs.

HOT TIP: If you want to move your money from one ISA to a more efficient ISA make sure you transfer directly! Avoid being charged tax by withdrawing and then depositing your money through another bank account.

Now you know all about the different types of ISA out there. What will you go for? Follow BullBear to stay up to date with the latest financial tips and tricks.